월트디즈니의 2022 Q1 어닝리포트를 분석해보도록 하겠다.

어닝자료는 디즈니 공식 인베스트 홈페이지에서 가져온 정보이니 오피셜이라고 보면 된다.

※ 오역 있을 수 있음

We’ve had a very strong start to the fiscal year, with a significant rise in earnings per share, record revenue and operating income at our domestic parks and resorts, the launch of a new franchise with

Encanto, and a significant increase in total subscriptions across our streaming portfolio to 196.4 million,

including 11.8 million Disney+ subscribers added in the first quarter,” said Bob Chapek, Chief Executive Officer, The Walt Disney Company.

- 강력한 EPS증가와 회계연도를 시작한다. 매출과 영업이익률 늘어났고, 지역파크 리조트 새로운 프렌차이즈 '엔칸토' 그리고 유의미한 스트리밍 포트폴리오 구독자 수가 1억 9,640만명으로 1180만명이 늘어났다.

This marks the final year of The Walt Disney Company’s first century, and performance like this coupled with our unmatched collection of assets and platforms, creative

capabilities, and unique place in the culture give me great confidence we will continue to define

entertainment for the next 100 years.

- 우리는 존나 쩐다. 우리는 향후 100년간 엔터테인먼트를 정의할 것이다.

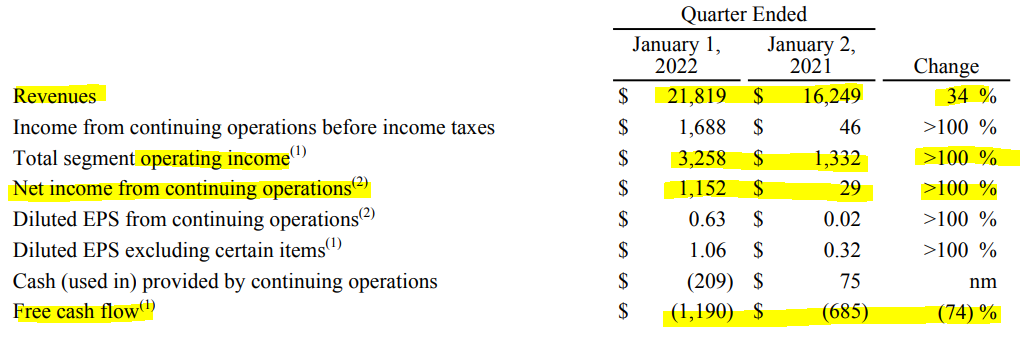

- 매출은 늘었고 영업이익률, 순수익도 늘었는데 FCF는 적자폭이 크다. 아직 투자를 많이 하고 있어서 그런듯.

- 우리는 코로나 시대에 살고있다. 코로나 때문에 뭣같다. 그런데 거의 많이 정상화 되었다. 그래도 여전히 뭣같은 부분들이 산재해 있다.

- 예전에는 세그먼트를 4가지로 분류하더만 이제는 2가지로 줄인것 같다. 에효

아무튼 스트리밍이나 영화 등 미디어 관련 무형적인 부분들은 1년새에 15% 매출상향에 그쳤고 영업이익률은 오히려 44% 역성장을 했네...

- 그리고 디즈니파크 및 여러 오프라인적인 측면들은 매출도 늘고 영업이익도 대폭 증가했으나 이건 뭐... 코로나가 풀리면서 풀린게 아닌가 싶은 느낌이라 크게 칭찬해줄만하지 않다.

- 미디어 엔터테인먼트 부문에서먼저 Linear Networks부문. 쉽게 말해 케이블 TV 부문으로 디즈니, ESPN, FX, 네셔널 지오그래픽, ABC같은 채널이 속하는데 뭐 유의미한 매출증가도 없고 오히려 영업이익은 떨어졌다.

- 그다음 DTC부문은 OTT부문을 가리키는데 디즈니+나 훌루 등을 의미하겠다.

여기도 매출은 늘어났는데 영업이익은 27%나 역성장

Direct-to-Consumer revenues for the quarter increased 34% to $4.7 billion and operating loss

increased 27% to $0.6 billion. The increase in operating loss was due to higher losses at Disney+, and to a

lesser extent, ESPN+, partially offset by improved results at Hulu.

- 매출은 34% 증가했지만 영업손실이 27%로 늘었다고 한다. 그 이유는 디즈니+때문이라고 하는데 훌루에서 좀 상쇄해서 그나마 이정도지 그거 아니었으면 더 ㅈ박았을거다.

Lower results at Disney+ reflected higher programming and production, marketing and technology costs, partially offset by an increase in subscription revenue. Higher subscription revenue was due to subscriber growth and increases in retail pricing. The increases in costs and subscribers reflected growth in existing markets and to a lesser extent, expansion to new markets.

- 디즈니+의 ㅈ박은 결과는 높은 프로그래밍, 마케팅, 기술적 비용때문이었고 이거는 구독자 수입의 증가로 조금 상쇄했다. 비용과 가입자 증가는 기존 시장의 성장과 새로운 시장의 성장을 반영한다. = 그러니까 성장중에 지출이 좀 있으니까 괜찮다 이거임.

- 이건 구독자수같은데 1년전에 비해 디즈니+는 전세계적으로 37% 늘었고, ESPN+는 76%, 훌루는 15% 늘었다고 한다. 디즈니플러스는 미국+캐나다는 18% 늘었고 전세계는 40% 늘었네. 그러니까 북미는 이제 구독할대로 구독해서 좀 둔화되는 느낌이고 전세계는 아직 빡빡 늘어나는 느낌이다. 아직 괜춘한듯.

- 머릿수당 구독료는 전체적으로 늘어나는 느낌이라 좋네.

이게 구독료를 늘린건지, 아니면 사람들이 구독 패키지를 업그레이드 한건지는 모르겠지만.

일단 북미의 구독비용이 전세계의 비용보다 더 빡세다는 정보도 얻을 수 있겠다.

- 마지막으로 컨텐츠 세일 및 라이센스는, 말 그대로 컨텐츠 라이센스팔이를 하는것 같은데 극장배급, 음원유통 등등이 있겠다. 그런데 이건 매출은 매우 늘었는데 영업이익은 또 떨어졌네.

The decrease in theatrical distribution results was due to losses on titles released in the current quarter, partially offset by income from the co-production of Marvel’s Spider-Man: No Way Home. Titles released in the quarter included West Side Story, Encanto, The King’s Man, Eternals, Nightmare Alley and The Last Duel. There were no significant titles released in the prior-year quarter. The Company incurs significant marketing costs before and throughout the theatrical release, which may result in a loss during theatrical distribution.

- 이게 떨어진건 최근 개봉된 타이틀들의 부진 때문인데 그나마 스파이더멘 노웨이홈으로 좀 상쇄했다. 엔칸토, 킹스맨, 이터널즈, 악몽의 앨리 등이 출시되었는데 주요 핵심 타이틀들이 아니라 비용만 많이 들었고 부진했다는 것 같다.

왜? 엔칸토, 이터널즈, 킹스맨 이런거 잘 안됬나?